| September 23, 2005 | science@berkeley lab | | lab a-z index | lab home |

|

|||

On Insurance Risk and Climate Change: An Interview with Evan Mills

|

|||||||||||||||

| Contact: Dan Krotz, dakrotz@lbl.gov | |||||||||||||||

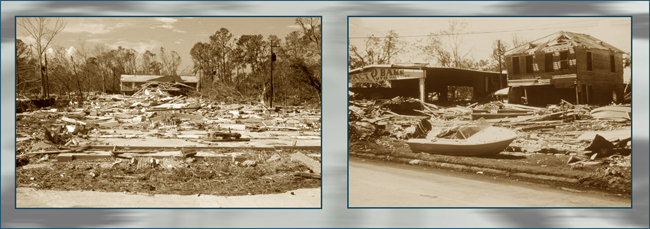

| Hurricane Katrina is expected to cause $35 billion in insurance claims, a sum the insurance industry will be able to shoulder. But what if the number of weather-related catastrophes is on the rise? Evan Mills, a scientist in Berkeley Lab's Environmental Energy Technologies Division, has spent more than a decade tracking evidence that the global insurance industry is paying out more in claims caused by extreme disasters such as hurricanes and forest fires. Like a growing number of scientists, he believes climate change is a factor.

If you're interest is in climate change, why focus on insurance? Mills: Insurers are an important part of society's climate observing system, integrators of the costs of weather-related hazards, and messengers of the implications through their pricing and terms. Insurance is also interesting in the broader political discussion because it represents a big industry — in fact the world's largest industry — that, unlike some others, sees climate change as a threat to its bottom line and sees action as less costly than inaction. What impact will Hurricane Katrina have on this issue? Mills: It has already had a profound impact, first by elevating the importance of continued scientific work to understand the driving forces within hurricanes, and their linkages to climate. It also has important near-term impacts in the marketplace, such as elevated insurance prices, increasing deductibles, reduced limits on payable losses, and insurer withdrawals from the market. Katrina highlights the interactions between human activity and natural disasters. In a very real sense, Katrina was not a true natural disaster. The damages represent the confluence of a perhaps natural event and extensive maladaptation and vulnerability of human systems. In addition, if climate change is boosting the power of hurricanes (by increasing sea-surface temperatures), the meteorological event itself is also unnatural in that respect. How relevant are weather-related natural disasters for climate change, and is there any evidence that the situation is worsening? Mills: Globally, we see about $80 billion per year in weather-related economic losses, of which $20 billion are insured. This is like a "9/11" every year. Weather-related losses represent about 90 percent of all natural disaster losses, and the data I cited do not include an enormous amount of aggregate losses from small-scale or noncatastrophic events such as lightning, soil subsidence, and gradual sea-level rise. Inflation-adjusted economic losses from catastrophic events rose by 8-fold between the 1960s and 1990s, and insured losses by 17-fold. Losses are increasing about 10 times faster than insurance premiums. The insured share of total losses has increased dramatically in recent decades, and variability is increasing. Weather-related catastrophes have clearly visible adverse effects on insurance prices and availability. Of particular concern are the so-called "emerging markets" (developing countries and economies in transition), which already have $375 billion per year in insurance premiums (about 12 percent of the global market at present, but rising), yet are significantly more vulnerable to climate change than are industrialized countries.

Increased exposures are heavily influenced by rising demographic and socioeconomic exposures. Yet, the rise in losses has outpaced population, economic growth, and insurance penetration. The science of "attribution analysis" is still in primitive stages, and thus we cannot yet quantify the relative roles of climate change and human activities. What is the significance of insurance companies identifying global warming as a problem? Mills: It's significant in that it recognizes that the future may be different than the past, which is a departure from the way insurers understand many of the everyday risks they deal with. This is no small point, as insurers must anticipate and financially prepare for losses in advance of their occurrence. It also opens up the notion that insurers can play a role in the most profound type of risk management. They can actually stem rising losses by helping society address a root cause — in this case climate change. There are two major ways to approach risks: reactive and proactive. Insurers do both. Examples of the former include things like raising rates, withdrawing from certain exposures (like areas where hurricane risks are high, or from an entire category of loss such as household flood or certain crop risks), and shifting risks to governments as insurers of last resort. But, I don't think being proactive is a radically new way for insurers to approach these kinds of problems. Insurers founded the original fire departments, building codes, and institutions like Underwriters Laboratories. The specter of climate change is still novel in terms of its scale, the long timeframe of the issue, and the truly global perspective required to address the root causes of these losses. It is no small challenge, and insurers and their regulators understandably have their hands full in dealing with many other issues. So, the good news is that insurers can use traditional tools to cope with these new risks. The challenge is that climate change presents an unprecedented set of risks and virtually all branches of the industry are vulnerable. How would you describe the insurance industry's stance on the scientific evidence for global warming? Mills: As for any large industry, there's no single answer. We still have a segment — much too large a segment — that hasn't thought much about climate change at all. This group doesn't yet have a strategy. Then there's the group, including but not limited to insurers convened under a United Nations Environment Programme Initiative, who are tracking it very closely and are truly concerned. And, lastly, there is a small and shrinking group that disputes or feels unqualified to evaluate the scientific evidence. I would say that the middle group fully accepts the authoritative findings of the Intergovernmental Panel on Climate Change that human activity plays a central role in observed and anticipated climate changes, and the first group is inclined to accept it when it's presented at a level they can understand and digest. Part of the challenge is bridging the scientific world and the financial world, which is what much of our research is about. Of note, the insurance regulators, through the National Association of Insurance Commissioners, have taken very great interest in the climate change issue of late. I expect to see very constructive action from that quarter, in terms of fostering better modeling and data collection and assessment of potential financial impacts.

How will climate change affect the average consumer trying to purchase homeowners or car insurance? Mills: As losses rise, so too will premiums. Similarly, deductibles can be increased or upper limits of coverage reduced. If done properly, this is appropriate. Like any industry, insurers need to cover their losses and generate a reasonable return for their shareholders. With the patterns of extreme weather events becoming more intense and more variable, the actuarial challenge will grow, and this will, in turn, put pressure on prices. More importantly, however, is the question of whether certain hazards will become uninsurable as has already happened, in part, with flood and crop risks related to weather. Questions along these lines are already being asked with regard to things like windstorm and wildfire. We also need to keep in mind that this issue isn't limited to property insurance. There is a very real link to insured business interruptions, highway accident rates, and various forms of liability insurance. Increased extreme weather events will also have impacts on health and life. So, the answer will reflect, in part, how the industry decides to respond. What I referred to earlier as the "reactive" strategies will tend to result in the greatest burden for consumers, whereas the "proactive" strategies will help reduce the long-term losses and maintain both the availability and affordability of insurance. Additional information

|

|||||||||||||||

| Top | |||||||||||||||